- 处理有解/x'x可逆的情况——非常简单的矩阵运算

- 补充上岭回归的惩罚参数a——也是简单的矩阵运算,也可以用梯度下降

- 交叉验证——计算平均预测误差 RMSE 在多次中的平均值

关键在于包装为成一个尽可能完整的class

Ridge 的封装——类

想要实现的功能:

- 划分训练和测试集

- 梯度下降迭代估计参数

- 绘制迭代cost收敛图

- 计算预测值

- 计算预测rmse

- 交叉验证的平均rmse

读入& 处理数据 & 提取变量

import os

import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

# 1.读入数据

os.chdir("/Users/mac/Desktop/快乐研一/python/data")

gaokao = pd.read_csv("高考待预处理.csv")

gaokao.head()

data = gaokao.iloc[:, [2, 3, 11, 4]]

data_x = data.drop(["分数线"], axis=1) # # 提取自变量——重点学科、博士点、是否为综合类大学

data_y = data[['分数线']] # 因变量——分数线

# 2.标准化

def biaozhunhua(x):

return (x-x.mean())/x.std()

data_y = data_y.apply(biaozhunhua)

data_x[["重点学科","博士点"]] = data_x[["重点学科","博士点"]].apply(biaozhunhua)

| 大学名称 | 类型 | 重点学科 | 博士点 | 分数线 | type_农业 | type_医药 | type_工科 | type_师范 | type_林业 | type_民族 | type_综合 | type_财经 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 北京大学 | 综合 | 81.0 | 201.0 | 694.0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 |

| 3 | 复旦大学 | 综合 | 30.0 | 178.0 | 687.0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 |

| 4 | 清华大学 | 综合 | 37.0 | 253.0 | 686.0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 |

| 5 | 上海交通大学 | 综合 | 9.0 | 78.0 | 664.0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 |

| 7 | 南京大学 | 综合 | 21.0 | 44.0 | 662.0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 |

具体实现(梯度下降)

- 岭回归也可以通过矩阵求逆直接计算

- 这里当做优化问题来做——梯度下降法

class Ridge():

def __init__(self):

self.w = None

self.b = None

self.costlist = None

self.epochs = None

# 1.获得参数估计值

def getParam(self):

print("\nW: {}\nb: {}".format(np.round(self.w,3), np.round(self.b,3)))

return self.w, self.b

# 2.计算梯度

def l2_loss(self, X, y, w, b, alpha = 0):

num_train = X.shape[0]

num_feature = X.shape[1]

y_hat = np.dot(X, w) + b

cost = np.sum((y_hat-y)**2)/num_train + alpha*(np.sum(np.square(w)))

dw = np.dot(X.T, (y_hat-y)) /num_train + 2*alpha*w

db = np.sum((y_hat-y)) /num_train

return dw, db, cost

# 3.迭代估计

def fit(self, data_x, data_y, learning_rate=0.05, epochs=1000, alpha=0, ifprint = False):

'''

输入:X、y、学习率、迭代次数、惩罚系数

输出:估计参数、cost(list)

'''

self.w = np.zeros((data_x.shape[1],1))

self.b = 0

self.costlist = []

self.epochs = epochs

for i in range(epochs):

dw, db, cost_tmp = self.l2_loss(data_x, data_y, self.w, self.b, alpha = alpha) # 计算梯度

self.w = self.w - learning_rate * dw # 更新参数

self.b = self.b - learning_rate * db

self.b = self.b.tolist()

self.costlist.append(cost_tmp) # 记录下cost函数的递减过程

if (ifprint==True) and (i % 100 == 0): # 打印训练过程

print("迭代次数:%d, cost=%f" % (i+1, cost_tmp))

if ifprint==True:

print("%d次迭代结束!最终训练集上cost:%f" % (i+1, cost_tmp))

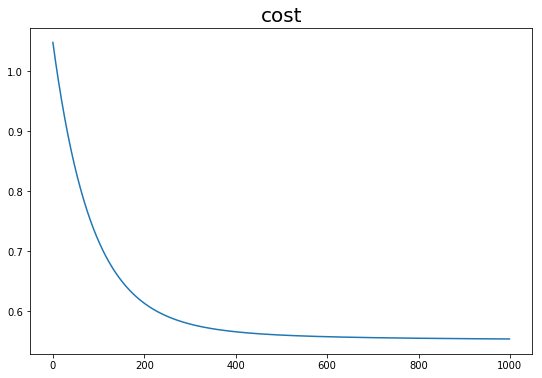

# 4.绘制cost收敛

def plot_cost(self):

fig = plt.figure(figsize=(9,6))

plt.plot(range(self.epochs), self.costlist)

plt.title("cost", fontsize=20)

plt.show()

plt.close()

#5. 计算rmse:

def rmse(self, test_y, test_pred):

x = np.squeeze(np.array(test_y))-test_pred

return np.sqrt(np.squeeze(np.dot((x).T,(x)))/len(x))

# 6.计算预测值

def prediction(self, test_x):

yhat_l2 = np.squeeze(np.dot(test_x, self.w) + self.b)

return yhat_l2

# 7.# 划分训练集和测试集

def sample(self, data_x, data_y, percentage=0.8):

sample = np.random.choice(range(len(data_y)), int(len(data_y) * percentage), replace= False).tolist()

train_x = data_x.iloc[sample, :]

test_x = data_x.iloc[[x for x in range(len(data_y)) if x not in sample], :]

train_y = data_y.iloc[sample, :]

test_y = data_y.iloc[[x for x in range(len(data_y)) if x not in sample], :]

print("训练集样本量:{}测试集样本量:{}".format(len(train_y),len(test_y)))

return train_x, train_y, test_x, test_y

### 测试 ridge 函数类

# 1.初始化

model = Ridge()

# 2.分割测试和训练

train_x, train_y, test_x, test_y = model.sample(data_x, data_y, percentage=0.7)

# 3.训练model

model.fit(train_x, train_y, learning_rate=0.003, epochs=1000, alpha=0.1, ifprint = True)

# 4.获取参数估计值

w, b = model.getParam()

# 5.绘制训练过程中的cost收敛过程

model.plot_cost()

# 6. 预测

test_pred = model.prediction(test_x)

# 7.计算预测rmse

rmse_l2 = model.rmse(test_y, test_pred)

print("\n 岭回归(惩罚系数0.1\n预测集上rmse={}".format(rmse_l2))

训练集样本量:89测试集样本量:39

迭代次数:1, cost=1.048072

迭代次数:101, cost=0.716701

迭代次数:201, cost=0.613186

迭代次数:301, cost=0.578509

迭代次数:401, cost=0.565609

迭代次数:501, cost=0.560109

迭代次数:601, cost=0.557384

迭代次数:701, cost=0.555831

迭代次数:801, cost=0.554838

迭代次数:901, cost=0.554142

1000次迭代结束!最终训练集上cost:0.553627

W: [[ 0.321]

[ 0.364]

[-0.05 ]]

b: [-0.052]

岭回归(惩罚系数0.1

预测集上rmse=0.7781370066362491

定义函数——普通最小二乘(矩阵求逆)

$rmse = \frac{(X\beta -y)'(X\beta -y)}{n} $

##### 正式定义函数——OLS

def my_OLS(data_x, data_y):

####### 1.构造数据 ######

# 在第一列插入1

col_name = data_x.columns.tolist()

col_name.insert(0, 'x0')

data_x = data_x.reindex(columns = col_name)

data_x['x0'] = [1] * data_x.shape[0]

####### 2.计算OLS估计量 ######

xTx = np.dot(data_x.T, data_x) # x'x

xTx_I = np.matrix(xTx).I # (x'x)的逆

beta = np.dot(np.dot(xTx_I, data_x.T), data_y)

beta = np.squeeze(np.array(beta))

####### 3.输出 ######

yhat = np.dot(data_x, beta)

return yhat, beta

# 测试

# train_x, train_y, test_x, test_y

yhat_ols, beta_ols = my_OLS(train_x, train_y)

yhat_ols = np.dot(beta_ols[1:len(beta_ols)], test_x.T) + beta_ols[0]

rmse_ols = model.rmse(test_y, yhat_ols) # 普通最小二乘rmse

print("普通最小二乘法参数:{} \n 预测集上rmse={}".format(np.round(beta_ols,3),np.round(rmse_ols,3)))

普通最小二乘法参数:[ 0.034 0.344 0.479 -0.029]

预测集上rmse=0.793